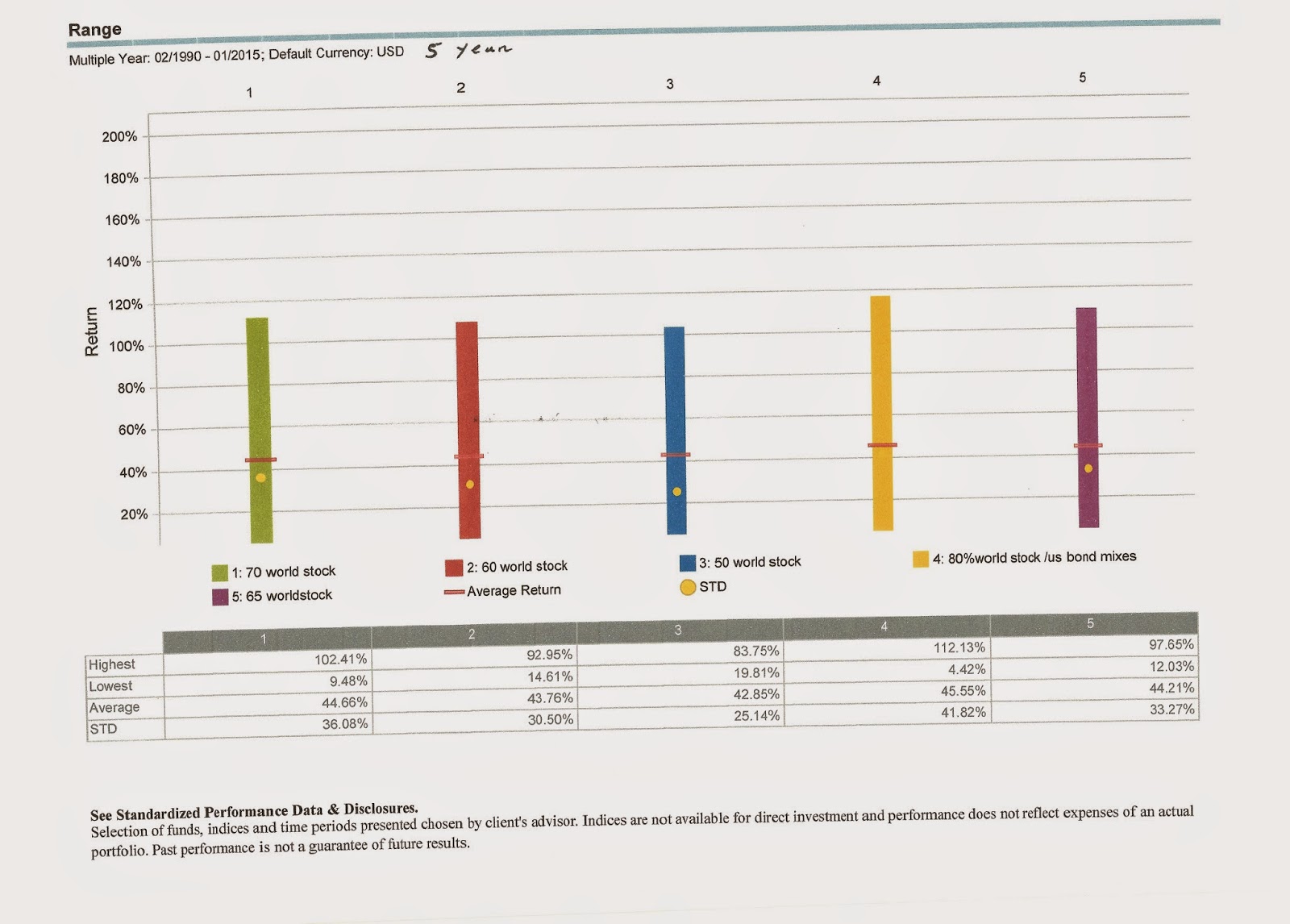

In

my first article on “robo advisors” I pointed out many shortcomings of the

“robo advisor” process. I detailed all the questions which the “advisor”

doesn’t ask which are essential to investment planning. I didn’t even discuss

the actual allocations proposed by these services and how they are implemented.

Reviewing

the allocations of the major robo advisors one finds widely divergent

allocations. Investing and asset allocation are at the end of the day a mix of

“art” and science. The differences among these portfolios are significant and

reflect very different views on investing.

But

somewhat ironically, the target market for these robo advisors is individuals

who have little interest in getting deeply involved in their investment choices

and are looking for a simple inexpensive way to allocate their investments. Yet

the assumptions inherent in the allocations are so complex that few if any

individuals in this target market” or indeed many non-professionals (and plenty

of professionals too) would have difficulty carefully analyzing these

portfolios.

Furthermore

since there is little explanation that I have seen on the websites of the

choices made in the portfolios, when or why they might make changes in the

portfolios or specific risks in the portfolios Investors are often buying a

portfolio they don’t really understand And since they must buy the entire

portfolio they can’t remove from the portfolio any asset classes they are

uncomfortable with.

And

the costs of these portfolios? The fees on these programs may be low but as

will be seen below that does not mean that the portfolios are really low cost

What’s

Under the Hood?

Do

you know what is under the hood? The various robo advisor portfolios contain

some weightings and choices that are certainly subject to debate in the

investing...

Etf.com

produced a great analysis going under the hood of robo advisors allocation. An

in depth analysis is in this article

I’ll

just highlight some of the differences

Some robo advisors include broad based

commodity exposure, some gold, some REITS, some have a long duration bond

portfolio some shorter, some include inflation protected bonds,

emerging market bonds, developed market international bonds and some don’t. On

the equity side the choices of instruments, type of allocation (market weight

or value tilt for example) vary widely. There are robo advisors that include

allocations to specific industries,

And

the differences in allocations are not a trivial matter, they are extremely

significant here is one example

Here

are the allocations in the 90% stock allocations for two Robo advisors

|

Betterment

|

Wealthfront

|

|

Developed

International

|

22%

|

38%

|

|

Emerging International

|

28%

|

10%

|

In

fact Betterment’s allocation to emerging markets stock is less than half that

of the other major robo advisors.

Obviously

this is a huge difference and just of one of dozens across all the major robo advisors.

How many individuals could make a judgment among

these or find a good explanation (as they should get from a good advisor) as to

why the allocation is as it is, how it has performed in the past and even what

long term expectations are. And of course in many cases working with an advisor

they could individualize the allocation after the details of various pieces of

the allocation are explained. None of this will be done by the robo advisor.

Here

is the ETF.com article’s analysis of the Betterment allocation I would doubt

many Betterment clients would be able to do this analysis, understand it and

evaluate it compared to alternatives. And Betterment says it is thinking of

adding more/different ETFs. How will the clients learn about this and when and

why?

From ETF.com:

Betterment has

come through on its pledge to deliver marketlike exposure with a value

orientation. But its promised small-cap tilt and downside protection are not in

evidence. Like Wealthfront, Betterment takes on moderately high duration and

credit risk from its muni bonds.

Betterment

pulls off the trick of being both marketlike and value-oriented while not

tilting small by making value allocations with U.S. equities only. U.S.

large-cap value funds emphasize mega-caps, so Betterment’s value tilt increases

its portfolio-weighted average market cap.

If,

in the future, Betterment ventures into international value funds, as Chief

Executive Officer Jon Stein suggested they might if expense ratios fall, its

portfolio-weighted average market cap would likely rise further, approaching

the global-weighted average, since mega-cap firms dominate value funds globally

Betterment

makes use exclusively of Vanguard ETFs certainly in terms of cost they are

usually a good choice and the lowest cost in most categories. But there is d an

expense ratio price war going on and ETFs from Schwab and Ishares now have ETFs

at expense ratios very close to Vanguard’s.

Methodologies differ, it could

certainly be that the fee difference is offset by differences in strategy. To

give a significant example several robo advisors use dividend oriented ETFs

which have widely different methodologies. It is not transparent why these

firms chose one vs another and would they explain their choices to you and if

and when they might make a change.

Several

robo advisors make use of industry sector funds. What are the criteria for

those choices? Do they ever change? If so why? This is another set of “under

the hood” issues many investors particularly the type that would use a robo

advisor will likely not ask...or even understand. And how would they even ask a

robo advisor and of course if the response is not satisfactory to the potential

Betterment investor he would have to move to another one since all the

Roboadvisors are “packages” that can’t be broken up.

Risks

you may not be aware of. In my view emerging market bonds are an asset class

that is not worthwhile to own given its risk/return characteristics. Others may

differ, but how many of those using Betterment (to give one example) know that it owns an

emerging market bond fund as 4% of their model allocation. The emerging markets

bond etf from Vanguard which Betterment uses has a 10% allocation to Brazil a

9.4% allocation to Russia and a 6.3% allocation to Turkey. How many Betterment

investors will be aware of this or check the holdings of each of the ETFs owned

in their portfolio to find this out? Investors buy the Betterment portfolio

as a package and don’t have the choices explained in depth. And the investor does not have the option

that he would likely have with an advisor to simply eliminate an asset class

from your portfolio after the risks are explained.

This

is just one example the same could be said to one degree or another about every

choice in every robo advisor portfolio. Will the investor know what particular asset

class performance affected the portfolio performance and is this explained to

you in any quarterly or annual reports…to the best of my knowledge there is no

in depth reporting explaining results.

Will

Investors Start to Chase Performance Among Robo Advisors?

Since the allocations of robo advisors differ the

performances of course will differ. Will investors be tempted to check performance across robo

advisors and switch based on short term performance? Certainly as these

products grow there will be articles reporting on the performance of the robo

advisors. I can predict Morningstar ratings on each of the robo advisors

will be coming soon. Investors will doubtless make investment decisons based on the Morningstar analysis. This despite the fact that Morningstar acknowledges (but you can’t find that

information very easily) that their “star’ ratings are not predictions of

future performance…and they change. Instead of simplifying things for investors

the growth of robo advisors will simply lead to a different level of

complexity.

Changes

in Response to Market Conditions

You

probably would not like to work with a “non robo” advisor that make frequent

changes to your allocation. But in my view there are some conditions where

strategic changes in portfolios are merited.

Here

is one important example: It is crystal clear that the next move in US interest

rates will be up. It is also a simple fixed relationship that the longer term

the bond the more its price is affected increases in interest rates. A “non

robo” advisor would often choose to reduce the duration of its bond allocation

under current market conditions. The robo advisors have varying durations in

their bond allocations…but none of them own only or mostly short term bonds.

Thisarticle presents a very thorough analysis of the impact of rising rates on the bond

market. I haven’t seen any indication that Robo advisors make adjustments to

their bond portfolio in light of the near certain increase in interest rates

(the only question is when…not if it will happen) Some non robo advisors will

make adjustments because of this and I am sure that most will explain this decison to their investors.

An informed consumer looking

at putting their life savings with an advisor robo or other should ask how the portfolio is positioned for a rise in interest rate. If they

asked a robo advisor who would answer? And of course the response to the answer

was unsatisfactory the consumer would have to move on to look at another robo

advisor

There

are other specific categories of ETFs that are likely to be unfavorably

affected by rising rates. Based on historical market performance these would include REITS and dividend stocks. How is the robo

advisor positioned now in response to the near certain increase in interest

rates? Why? And what changes might the robo advisor make ant why.

There

is much more to say about looking “under the hood” of robo advisor portfolios.

After doing due diligence an investor would likely find choices in virtually

every allocation that it would prefer not to be in its portfolio. Investors,

certainly those in the target market for robo advisors who “want a simple

solution to their problem of how to allocate their money may not be getting what they are looking for.

It is unlikely they

would be inclined or have the skills to do thorough analysis and due diligence

in reviewing robo advisors. In fact these investors would be the least likely

to have the skill or inclination to make such analysis.

To

do a thorough review they would likely have to pay a “non robo” advisor to help

them. And even after that review of the robo advisors many may find that

picking the best solution to meet their needs is a bit like solving a Rubik’s

cube in fact it is even harder if not impossible.

Since you have to buy the

“package” with a robo advisor there will almost inevitably not be a robo

advisor that perfectly matches an informed client’s preference. But a good “non

robo” advisor would be able to customize client portfolios rather than using

what is virtually a one size fits all approach.

Trade

Execution: There are more costs than just the management free.

It

is unclear how the robo advisors execute the trades in their portfolios. Money

will be coming in every day. Do they execute all the trades at one fixed time

every day? How do they do their rebalancing trades? If the markets are

particularly volatile on a particular day do they restrain from trading, do

they make sure not to trade on the day or time of major economic events, what

controls do they have for something like a “flash crash” or extreme moves in a

particular asset class or sector they own.

I

am sure the robo advisors don’t all use the same methodology. But how many robo

advisor consumers would know to ask or fully understand the implications for

the investor. And how many robo advisors will disclose that information?

Why

is this important? Because the differences in trade execution can create

unnecessary costs to the investor far in excess of the explicit robo advisors

fees.

The

article notes that differences in execution “could save you from trading

at a price that could eat up a year’s worth of return on a stock”

Now consider the case of

the robo advisor who needs to execute millions or tens of millions of dollars

of purchases or sales of a particular security. Not only would it be hard to

enter the trades with a “marketable limit order” as recommended in the article.

The orders themselves could “move the market” making the trading price less

attractive than it was when the trade was about to be executed.

Now consider the not likely scenario (in fact it has already existed) that it becomes knowledge in

the market that a large robo advisor executes its rebalancing trade the 15th or

every month at noon. It is not hard to figure out what the trades will be. The

details of the allocation are public and the particular trades are clear. The

robo advisor will be selling what has gone up and buying what has gone down.

Not only are human traders savvy enough to take advantage of this there are

high frequency traders whose entire business is built upon making profits

because of short term activity in the market.

Trades like the one

described are a big fat pitch down the middle of the plate for human and robot

traders to make money at the expense of the robo advisor.

A human advisor would have

far little if no “market impact” since their trades will in almost every case

be far smaller than the robo advisors. And the human advisor can fine tune his

execution.

And this problem will only

increase over time if the robo advisors continue to gather assets. Betterment

alone has close to $1 billion in assets under management is in very early

stages and is just starting to gain awareness among the general public through

exposure in the mass market press I am sure that few if any of the issues above

are discussed in these articles.

Despite the many issues

related to robo advisors virtually all of the articles in the popular press praise the robo advisors as the “wave

of the future” and praise them as the best choice for investors because of

their low costs.

This blog entry and my

previous one has reviewed many and far from all of the issues and hidden costs

associated with a robo advisor. Etf.com has published several articles which

analyze various issues related to robo advisors. And even though the new blog

articles together are fairly lengthy I have covered only a small number of the

relevant issues

Perhaps the apparent

savings and utility of using a robo advisor are illusory and a one size fits

all stock amd bond allocation is not the best choice. In fact perhaps it makes

sense to find “non roboadvisors" to work on a consulting basis or asset

management of an ETF portfolio for a reasonable fee…even if it seems higher

than the ultra-low cost robo advisor