The answer is a resounding no….which is the case for an

investor in the Unites States, Germany. Hong Kong or Brazil if the issue is

whether to invest only in home country stocks…but is even more the case for

those living in Israel. Given the small size of the Israeli economy and

domestic market and the fact that the most successful Israeli companies are

global companies with their stocks largely traded on the US markets…the

argument against holding a significant part of investment portfolio in Israeli

stocks is even stronger. That is certainly the way insurance companies and

other institutional investors set their stock allocation the number that invest

100% in their domestic market is quite small.

·

All investors should have

global diversification(

see wsj here). It is abundantly clear that we are in a global economy

and investing in just a small part of it doesn’t make sense. Investors around

the world suffer from a “home country bias” investing the overwhelming part of

their portfolio in their home country and missing the benefits of global

diversification. Even for US investors living in the home of the world’s

largest economy and capital market

experts recommend holding between 20 -30% of

one’s portfolio outside of the US. And the US market represents just under 50% of the worlds market capitalization

Israel represents .30% of the world's stock market capitalization. This means an investor invested 100% in the Israeli stock market holds only .30% of the stocks available for investment globally.

Now to the specific case of the Israeli investor where the

case for the overwhelming amount of one’s stock holdings outside of Israel

makes sense.In fact Israeli pension funds which hold 60% of their assets in Israeli government bonds invest over 40% of their non government bond assets outside of Israel.

·

First off …what is a “truly

Israeli company ? Israeli is a tiny

economy but home to many successful corporations. Many of these are world class

corporations…but to call them what I would designate in this article as “truly

Israeli companies” would be a misnomer. They are global companies some

headquartered in Israel (and many not) with operations around the world. The overwhelming

percentage of their sales and operations take place outside of Israel and their

economic performance is contingent on

factors in the global economy and trends in their industry, not the Israeli

economy.

In fact most of those companies are either not listed at all

on the Tel Aviv stock exchange or are “dual listed” on one of the US exchanges

as well as the Tel Aviv exchange. It is the US stock exchange where the trading

takes place and the global stock price is established…and it is a price in

dollars even if it appears in Israeli shekels on the Tel Aviv Stock Exchange.

and there is absolutely nothing going on in the Israeli

economy, financial markets or currency exchange rate that has any relevance to

the prospective deal and its impact on the economics and future stock price of

the two companies. Yet Perrigo and Teva both dual listed and are the 2

largest components of the Tel Aviv 25 stock index. Together they make up 20% of

the index.

What are the other major companies on the Tel Aviv stock

exchange ?

The Israeli stock index the Tel Aviv 25 has a very high

weighting in multinational corporations. In addition to Teva and Perrigo, Nice

systems and Elbit 2 world class corporations in the technology area make up

another 10%. Again as in the case of Perrigo and Teva very little in the Israeli economy is important to the economic fate of these tow companies.

So

what are the truly “Israeli” companies in the index? I

would define a “truly Israeli company” as one having the vast majority of their

business, revenues and earnings in Israel in local currency and local economic

and political conditions in Israel a major factor affecting their economic

fortunes. Looking at the rest of the index. one

finds 25% in the financial

sector, 8.5% in the real estate sector and 11% in energy. The full weightings of the index can be

found

here:

And looking at these industries it is possible to identify some

significant risk factors particularly because of local economic conditions and

political conditions. The financial services industry is extremely

concentrated and the incoming Finance Minister has set reform of the banking

system to bring more competition into financial services as a top priority.

The real estate

markets fortunes are highly determinant on Government policies. Given the

huge run up in real estate prices in the last 7 -10 years there is great

financial pressure for government activity to slow or reverse the trends in

real estate prices. Because of many complications in the nature of real estate in Israel government the government role is central.

And of course developments in the financial and real estate industries in all countries are intertwined.

As for the third major sector :The energy industry in Israel's future fortunes are highly dependent on development of the large offshore natural gas projects...and government policy has massive impact on that project.

Israel Chemicals (ICL) is a bit over 6% of the index and it too is highly dependent on changes in government regulations.

To illustrate the impact of changes in government regulation: Between Jan 1 2011 and July 31,2012 Cellcom, which pre market liberalization was the dominant player in the the cellphone market which had been tightly regulated lost 81% of its stock value. This was the period in which deregulation came to the cellphone market. At the time cellphone companies has a very high weighting in the Israeli stock indices. EIS, the Israel ETF lost 32.7% in 2011.

Added together the picture can be seen as follows: an

Israeli stock market dominated by two large multinational companies and sectors

that may be subject to the major impact of future government policy.

Looking at the above list it is hard to make a strong

investment case for investing in Israeli companies particularly for those who

already through their home ownership have a large exposure to the fate of

Israeli real estate. Add in the risks related to possible changes in economic

policy and the reality of being located in an unstable political/military

environment and the rationale for holding a significant proportions of one’s

equity holdings in specifically Israeli companies is very weak.

High tech Israel is not on the Israeli stocks exchange.

Israel definitely has a high tech sector whose success is impressive far out of

proportion to its position in the world economy. But that success creates high

investment returns for venture capitalists who invest in Israeli start ups at

their early stages and a small number of principals in the companies. Those two

groups make their money when one of 2 things happen:1.the corporation is bought

out by a major multinational company as was the case for be Waze which was purchased

by Google in 2013 for a reported $1.3 billion.Or 2. When the company goes public

on the US stock exchange A recent

example would be Mobileye (MBLY ) which went public on the US Nasdaq in 2014 and is not even

listed on the Tel Aviv exchange.

In both of those cases the big profits are made well before

investment is open to individual investor on the public market. Even when it

becomes possible to invest in the company after it becomes publicly traded.by

that point it is simply another tech stock. And of course its fate is

determined by the global factors affecting other corporations in its

industry….it is certainly not an “Israeli” company economically.

In sum the universe of “truly Israeli companies” i.e. corporations whose economic fate is primarily determined

by the Israeli economy and market is a very small one. And the investment case

for them does not appear to be particularly compelling.

An analyst from Barclays made the same point in this excellent article from 2012 explaining the sharp drop in volume on the Israeli stock exchanges.

Joseph Wolf of Barclays Capital: ...

“A major issue is the fact that 50% of the new money invested in equities by (Israeli)institutions such as pension funds is going overseas.” Wolf does not necessarily blame the domestic institutions for turning their backs on their home market: “Key sectors of the Israeli market, such as telecoms, banks and oil companies, have all been made much less attractive to foreigners and domestic investors because of regulatory or legislative intervention over the last two years.”

The unusual rules affecting investments by dual US Israeli

citizens creates a bit of a paradox. An investor interested in purchasing the

Israeli stock index would be best off doing it with a US traded etf ticker

symbol EIS and avoiding the PFIC problem related to taxing of non US mutual

funds and ETFs. The holdings of this ETF are also highly concentrated. T

he index used for EIS differs from the Tel Aviv 25

has a 24% weighting in TEVA and

a 36% weighting in financials.

Since the holding of individual stocks does not trigger PFIC

rules an investor interested in owning what are closer to “truly Israeli

companies “such as Bank Leumi, real estate developer Azrielli and food giant

Osem (all of whom also have significant foreign operations) could put together

a portfolio of those individual stocks. I wouldn’t think this is an attractive

alternative for most investors.

So what is a possible strategy for the long term Israeli

investor:

A long term portfolio should be diversified producing long

term returns from capital appreciation, interest and dividends with a mix of

stocks and bonds.

The stocks are designated to produce the long term capital

appreciation as the riskier part of the portfolio. The bonds producing mostly

interest income are expected to provide the stability in the portfolio less

return but less risk/volatiltiy.

There is a strong argument for a relatively small

allocation to Israeli stocks in the equity portion of the portfolio based on

the analysis. For US/Israeli dual citizens the easiest alternative for

most investors is the Israel ETF traded on the US stock exchange The rest of

the portfolio should be invested much the same as any other investor anywhere a

globally diversified portfolio invested in low cost index funds/etfs

What about currency risk? Certainly holdings in non

Israeli stocks (and stocks of Israeli global companies) exposes the Israeli

shekel based investor to the variations in the value of the Israeli shekel.

Just as in the case of global diversification in equities a strong positive

case can be for gaining he currency diversification as well.

In the long run currency fluctuations probably balance out over the long term. Furthermore the absence of

truly “Israeli companies” means that virtually all Israeli companies are

effectively dollar based.

There are Israeli mutual funds and etfs that hedge out

currency risk. Unfortunately they have two large drawbacks.The first is the

“dreaded PFIC problem” Israeli funds and ETFs create high taxes and reporting

headaches for US investors. The second is that those hedged instruments don’t

do a good job at executing the currency hedging.

Probably the best way to reduce the currency risk of the

portfolio is to alter the mix of stocks and bonds in the portfolio.

Many Israeli investment analysts and advisors recommend

holdings of non Shekel denominated bonds and even direct ownership of foreign

currency. My view on the holding of foreign bonds for the Israeli investor is

the same as my advice for the US based investor. The risk reward of such bonds

is unattractive. Instead of reducing volatility through the bond allocation

adding foreign bonds adds additional risk factors.

What is an alternative portfolio allocation strategy.?

Global stocks + domestic bonds.

Combining a global stock portfolio for long term

capital appreciation could make up the equity portion of the portfolio. The

bond allocation designed to provide steadier less volatile returns and reduce

the volatility of the portfolio could be allocated exclusively to high quality

Israeli shekel denominated bonds nominal or inflation protected. In order to

avoid the PFIC issue individual bonds and not funds must be used.

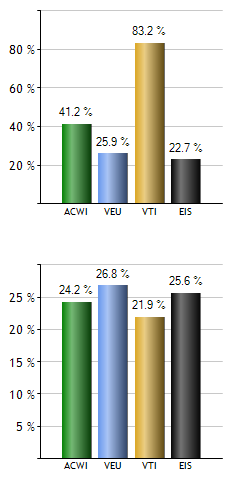

A note on past performance. Although I would base my choice of allocation more on the arguments above than past performance, the Israeli ETF has underperfromed the US, world ex US, and World stock market indices since its inception in 2007. Charts below growth of 100% and performance and volatility. You can not the large decline in 2011 largely due to the collapse of prices of cellphone companies was the major cause of the underperformance.

|

Growth of $100,000 Jam.1.2011 to May 12,2015 US total market (gold) World ex US (green),

total world market (blue) Israel (black)

|

|

Total Return (top) and volatility (bottom) Jam.1.2011 to May 12,2015 US total market (gold) World ex US (green),

|